What a move! I wrote last week that we were on the cusp of a potential break higher in the grain markets, but the move in wheat this week was beyond impressive, I must admit. In fact, it was the biggest weekly move in wheat in 2 years! The funds have held a significant net short since then with many rallies expected to be the big one only to fail miserably followed by new lows. Not this time.

The fact that May wheat, corn and soybean options expired Friday also has some influence, but the drought in western Kansas, slow pace of wheat harvest in India and buying to refill the State Grain Reserve that is at a 16-year low were the primary drivers. Such fundamental concerns combined with a large net short led to short covering by the funds that further fueled the rally. Rarely do we get wheat markets rallying 7-consecutive sessions without a correction, but that’s what we’ve just experienced.

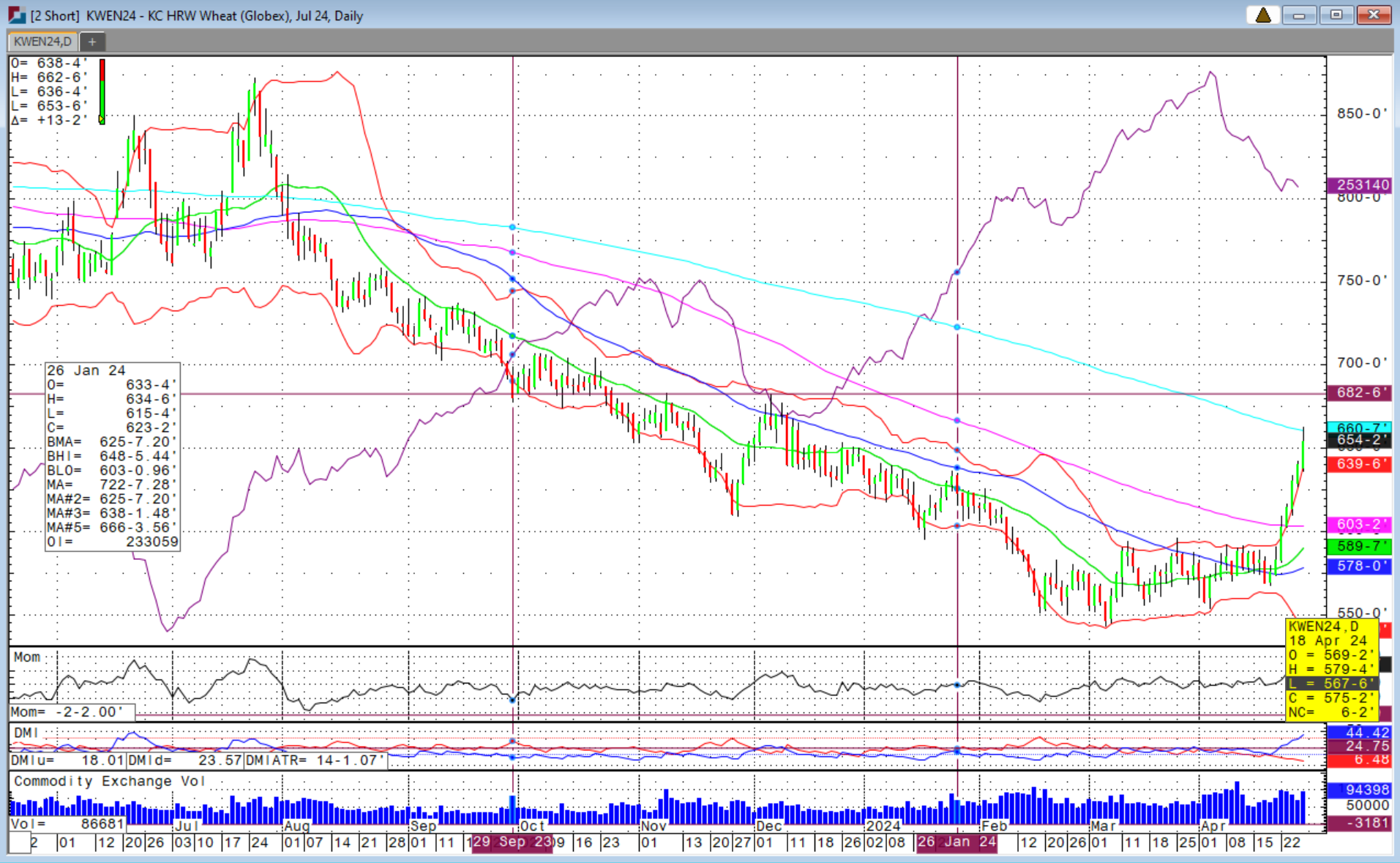

July Kansas City wheat surged from $5.67 ¾ low on April 18th to a session high on Friday at $6.62 ¾, 95-cent rally, before easing back into the close to finish the week at $6.54 ½. Chicago wheat quickly followed rallying from $5.50 to $6.33 ¼ on Friday closing at $6.22 ½. Both KC and Chicago wheat traded Friday above their 200-day moving averages for the first time since late July 2023.

July KC wheat 7-consecutive rally 95-cent rally

While parts of the wheat belt have seen rain this past week, there are still plenty of key areas where forecasts of heavy rains by meteorologists have not materialized. There are plenty of forecasts for Friday evening through Sunday calling for precipitation across the southern plains and Midwest, but western Kansas still looks to remain dry.

With that said, another disappointing few days of rains could see the July KC futures reach the $6.80-level last seen in early November and early December 2023. The Chicago wheat equivalent would be around the $6.50-level.

Winter wheat conditions this past week came in lower than expected at 50 percent Good-to-Excellent versus 54 percent expected. Kansas alone was down 7 percent week-over-week while Oklahoma was down 11 percent. Oklahoma could see some stability in next Monday’s rating, but Kansas could see further declines. While the current crop conditions overall are well above last year’s 26 percent G/E at this time, Kansas is currently at 36 percent versus 14 percent last year. That gap sure could continue to narrow and quickly change the optics of a ‘better-than-last-year’ situation. Nebraska and Texas were also down 2 percent G/E this past week, but still well above last year conditions.

With crop maturity running around two weeks ahead of normal, rains and cool weather at this stage will help with quality and test weight, but will have limited benefit of adding yield. Freeze damage is also beginning to show up more visibly in many fields with the combination of flash droughts and cold temperatures late compounding the impact.

The US dollar sure hasn’t provided any relief for US exports with the index surging higher Friday after the Fed’s key inflation measure of the core Personal Consumption Expenditures (CPE) price index, which excludes food and energy, came in at 2.8 percent for the month of March that was slightly higher than expected. Spending by households increased while savings decreased signaling robust consumer confidence that could keep inflation elevated and the optimism for rate cuts dampened. We will hear Fed Chair Powell’s latest updates after the next FOMC rate decision on Wednesday, May 1st.

Equity markets were choppy this week after US economic growth in the first quarter slowed to 1.6 percent, well below expectations, but finished higher after a large number of corporate earnings were released with more to come next week. Crude oil rebounded throughout the week with tensions heating up again in the Middle East.

With the confluence of everything aforementioned, it seems to me that the corn market is a sleeper with potential to make a move higher. The US corn crop is 12 percent planted, in line with expectations and ahead of the average 10 percent. While faster plantings can put downward pressure on the market, it is early and we could see weather premium return to this market depending on how the coming 3-4 weeks shape up.

Soybeans are 8 percent planted, also ahead of average and slightly ahead of expectations. Argentina soybean harvest continues to be delayed and is now well behind the average and last year. This could provide some support to the market. Soybeans are also at a potential area of strength, but need to trade above the 50-day moving average above before any meaningful upside is seen.

US grain exports this week were sold with corn better than expected, now at a 10-week high while wheat sales were mainly new crop. Soybeans were lackluster, which is not a surprise given buying is focused on the Southern Hemisphere this time of year given it is harvest there.

The cattle market traded both sides this week, but finished with impressive strength. Markets gapped higher on Monday, but closed off the highs and traded lower on Wednesday and Thursday filling gaps. With the selloff in equities after the US GDP numbers, I was expecting more of a selloff in cattle futures. Packer margins are weak and there is said to be ample beef supply, but fed cattle cash trade re-emerged late this week reaching $184 in Kansas on Friday morning and $186 later in the day in Nebraska.

April feeder futures and options expired Thursday settling at $244.875. May feeder futures are now the front-month and could be heading back to $250.000, the crossover of the 50- and 200-day moving averages, from Friday’s close at $248.250. Cash markets remain strong and summer grilling demand is happening now although it has been slow to ramp up. If corn markets break higher, that could create some headwinds for a further surge in cattle, but strength in the cash market may continue to bring resilience to this market.

If you’re buying cattle here, I do think it is prudent to protect them or at least some of them, but keep your upside open. This market will be volatile and the coming months are going to be particularly volatile with headline risk, buying returning to grain markets and geopolitical tensions that quickly impact equity markets as a demand barometer.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall.

If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available.

It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at http://www.sidwellstrategies.com/disclaimer.

On the date of publication, Brady Sidwell did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.